Creating a Project |

|

Creating a Project |

|

When you create a project that uses the FinOptions API component, a reference to the FinOptions 3.1 Type Library should be added to it. This library contains classes to price and value over 60 different types of derivative instruments.

This example, written with C#, shows how to price a vanilla option with the Black-Scholes model.

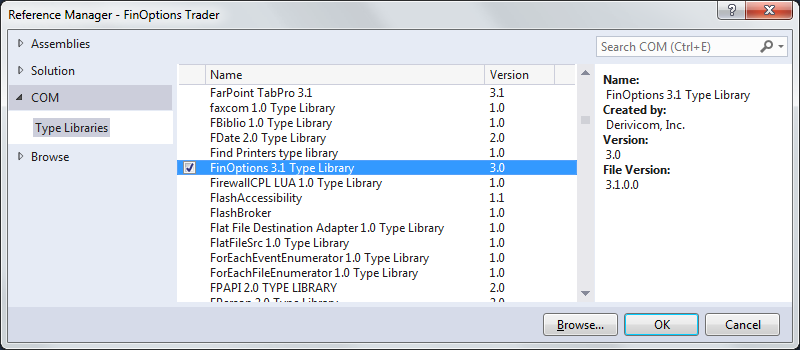

1.Reference the FinOptions 3.1 Type Library through the Add Reference option off of the Project menu.

|

2.Open a file that contains a form's declaration: in C# - a form's declaration can be found in the Form1.cs file, while in Visual Basic - the form is in the Form1.Designer.vb file). The form is declared as follows.

public partial class Form1 : Form { //... } Partial Class Form1 Inherits System.Windows.Forms.Form '... End Class |

3.Rewrite this declaration as follows. Please note that the attributes for the various parameters of the function would not be hard coded as below, this is done for demonstration purposes only.

private void Form1_Load(object sender, EventArgs e) { FinOptionsLib.VanillaOptions options = new FinOptionsLib.VanillaOptions();

} |

4.Then rebuild the project.

Object Model Overview

The library is broken down into four Class objects

Class |

Description |

||||||||||||||||||

ExoticOptions |

Provides a group of functions for pricing and valuing exotic options and their sensitivities. |

||||||||||||||||||

VanillaOptions |

Provides functions for pricing and valuing vanilla or standard options and their sensitivities. |

||||||||||||||||||

Registration |

Provides access properties to check the registration and register the software.

The following properties exist on the Registration object

|

||||||||||||||||||

Utility |

Provides utility functions to augment the financial models with functions to calculate historical volatility, interpolate and curve fit data sets. |